Tax-exempt Advance Refunding Overview

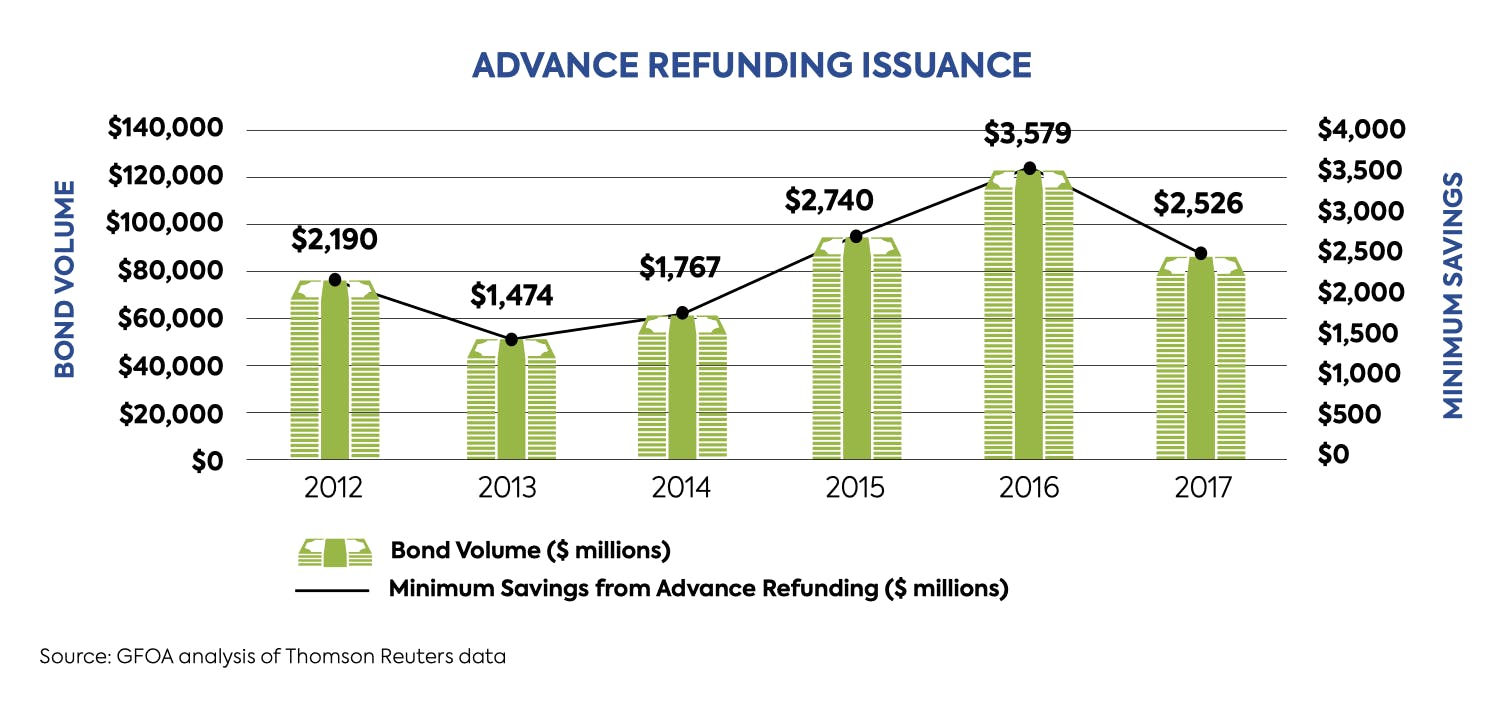

Tax-exempt advance refunding bonds allowed states and localities to refinance existing debt with the greatest flexibility, resulting in substantial reductions in borrowing costs. The elimination of advance refundings in the 2017 Tax Cuts and Jobs Act (TCJA) as a cost-savings tool for state and local governments has limited the options to refinance debt, especially since interest rates will certainly fluctuate over the lifetime of outstanding governmental bonds (which in many cases is 30 years). Advance refundings represented 27% of municipal bond market activity in 2016 and 19% in 2017. As a result, state and local governments are now paying more in interest, a cost that must be paid by state and local residents.

Furthermore, in addition to eliminating tax-exempt advance refunding, the TCJA decreased the overall corporate tax rate from 35% to 21% and ended other tax incentives that could impact overall demand for municipal bonds. Market experts are keeping a keen eye to see how the market will react to possibly reduced supply, less demand due to corporate tax changes, or perhaps increased demand by individuals who are looking for tax exempt products to help alleviate tax exposures due to new state and local tax deduction limits. Governments should be aware of these market dynamics as they consider going to market and determine appropriate action with consultation of outside professionals.

Despite being just weeks into the 119th Congress, we already have a bipartisan House bill to restore tax-exempt advance refunding. Reps. David Kustoff (R-TN-8), Rudy Yakym (R-IN-2), Gwen Moore (D-WI-4), and Jimmy Panetta (D-CA-19) joined together to introduce H.R. 1255. We encourage GFOA members to ask your Representative to cosponsor this bill. Additionally, we will work to have a companion bill reintroduced in the Senate as well.

Brief Legislative History

The 115th Congress saw the first bipartisan effort to restore tax-exempt advance refunding to the federal tax code. But in the 116th, efforts to restore advance refunding witnessed even more substantial support and progress. Bills were introduced in both chambers and in the House, the bipartisan bill to reinstate tax-exempt advance refunding was incorporated into the infrastructure bill that was passed by the House on July 1, 2020.

In the 117th, legislative efforts were quickly resumed as the bipartisan Senate bill was reintroduced - S. 479, the Lifting Our Communities through Advance Liquidity for Infrastructure (LOCAL) Act - by Sens. Roger Wicker (R-MS) and Debbie Stabenow (D-MI). Subsequently, the Co-Chairs of the House Municipal Finance Caucus (Dutch Ruppersberger (D-MD) & Steve Stivers (R-OH)) reintroduced their bill - H.R. 2288, the Investing in Our Communities Act. Further, Congresswoman Terri Sewell introduced H.R. 2634, the Local Infrastructure Financing Tools (LIFT) Act, that among other municipal bond provisions, includes a restoration of tax-exempt advance refunding. The provision was also included in the House-considered Build Back Better Act, but was not ultimately taken up by the Senate.

The was revived for the 118th Congress with the introduction of the Investing in Our Communities Act (H.R. 1837), led by Reps. David Kustoff (R-TN) and Dutch Ruppersberger (D-MD) in the House and the Lifting Our Communities through Advance Liquidity (LOCAL) for Infrastructure Act (S. 1453), led by Sens. Debbie Stabenow (D-MI) and Roger Wicker (R-MS).

Feel free to share this brief whiteboard video explainer!

RESTORE TAX-EXEMPT ADVANCE REFUNDING BONDS

Talking Points:

Urge Congress to reinstate the authority to issue tax-exempt advance refunding bonds.

- The 2017 TCJA repealed this critical cost-savings tool for state and local governments and has limited the options to refinance debt, which could free up capital and be put to immediate public works purposes.

- Having the option to refinance debt is a valuable financial management tool especially since interest rates will certainly fluctuate over the lifetime of outstanding governmental bonds (which in many cases is 30 years). Without tax-exempt advance refunding bonds, state and local governments will pay more in interest, a cost that must be paid by state and local taxpayers.

- Support legislative initiatives like H.R. 1255 in the House and similar bills in the Senate by cosponsoring them and calling on leadership in both chambers to advance this critical legislation to reinstate advance refunding bonds. Both bills would fully reinstate tax-exempt advance refundings, including private activity bonds and qualified 501(c)(3) bonds.

- 10-year revenue effect estimated at ~$9 billion.